Asset owners that are long-term investors should be wary of the conventional model of assessing the stock-bond correlation that is based on several “implicit assumptions”, said Stanford University Professor of Finance John Cochrane.

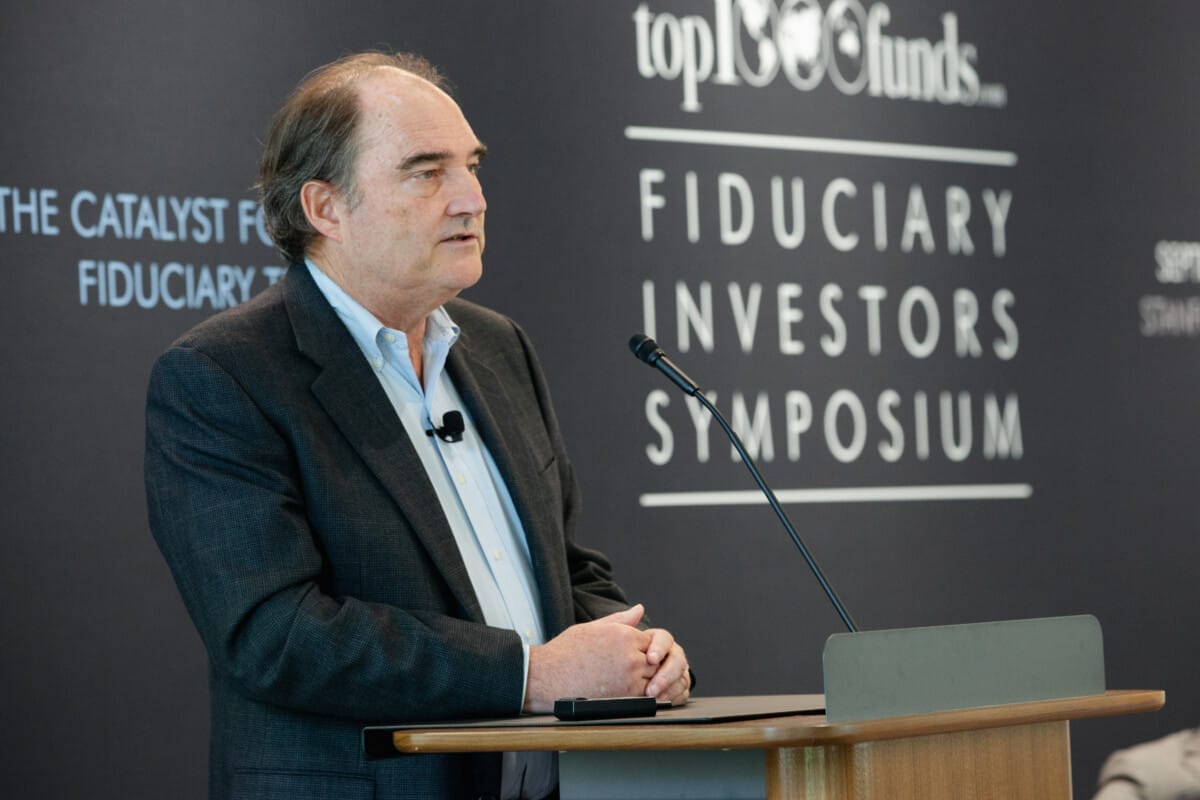

In a keynote speech at the Fiduciary Investors Symposium, Cochrane instead proposed a method that considers the economic situations which determine bonds’ status as a hedge or a risk.

Investors are conventionally trained to use statistical models to determine stock-bond correlations and look for the time-varying alphas and betas relative to that correlation, Cochrane said, but this model assumes a particular type of investor.

“You are assuming you’re talking to – or you are – an investor who cares about the mean variance of your portfolio, who holds only the market portfolio of stocks, has no job, no income, no liability stream, and cares only about one year,” Cochrane, who is also a senior fellow at the Hoover Institution, said.

“That’s a particularly bad assumption about bonds, because the one thing you need to know about bonds [is] when the price goes down, the yield goes up. A long-term bond, when you suffer a loss, you know it’s going to make it up in the long run.

“For a long-run investor with no immediate cash needs, who cares about mean variance?”

Cochrane encouraged the symposium to instead look at economic events when bonds were either hedges or risks, and to think about if they would have wanted to hold bonds ahead of time and how much they would be willing to pay.

“Just hedges or risks is not alone the question; the question is, are you the one who should be hedging or taking risk more than everybody else, because the average investor holds the market portfolio,” he said.

“I like to think about that in terms of fundamentals: where am I relative to everybody else who’s driving prices, rather than just statistical models, which I have learned over many years not to trust.”

The 2008 financial crisis is a classic case of bonds as a hedge, Cochrane said, because with inflation and interest rates both down, long-term government bonds got both a price and a real value boost “just as everything else was falling apart”.

But he said long-term bonds are risks when inflation comes into the picture, referencing how the $5 trillion US government fiscal expansion during COVID has been a “catastrophe” for long-term bond holders.

“The US government printed up $3 trillion, borrowed another $2 trillion, and sent it out as cheques to people,” he said.

“Whether good or bad, that $5 trillion, about half of it came from a 10 per cent haircut on long term bonds.

“The risk that happens is inflation. The risk that happens is the government decides we’re going to inflate away some of your debt in order to pay for something important.”

Instead of thinking about stock-bond correlations as fixed facts, Cochrane said investors will be better off with a simpler mindset – which is finding a stable economic structure and “understand changing times being we have different kinds of shocks”.

Responding to an audience question about the research view that it is the volatility of inflation and growth – instead of the level or the direction of them – that determines the stock-bond correlation, Cochrane said whether people need to care about it depends on what kind of investors they are.

“If you’re in a microsecond, millisecond, highly leveraged trading, short positions, long positions, posting collateral [kind of role], then you got to worry about these high frequency correlations,” he said.

But for long-term investors, “setting up the portfolio and thinking about the economic risks that your clients can handle should take more time than buying and selling at high frequency,” Cochrane said.

Leave a Comment

You must be logged in to post a comment.